Digital Transactions Authoritative, insightful and timely information for payments professionals

Digital Transactions Authoritative, insightful and timely information for payments professionals

Acquirers and independent sales organizations wanting to improve their standing among merchants should take note of four trends affecting payments today, according to Bill Dobbins, head of acquiring and enablement at Visa Inc.

Dobbins, speaking at the Western States Acquirers Association conference in Las Vegas this week, outlined why the consumer experience, small-business expectations, fraud shifting to online channels, and government regulation stand out for the impact they’re having on the merchant-sales industry.

“I’ve been in the payments industry for over 30 years now, the last 27 with Visa, and I can confidently say that the amount of change that our industry is going through now is more significant than any time in my career,” Dobbins said.

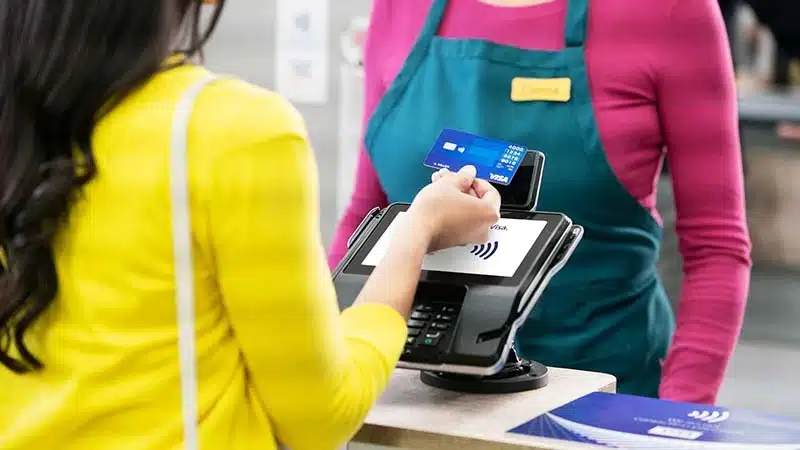

First up, consumers and their changing expectations. Chief among these is that consumers are demonstrating they like to tap to pay, Dobbins said. Fifty percent of Visa’s U.S. face-to-face transactions are made via a tap, Visa said in its latest earnings call.

Another element is that consumers like their payments easy. “Complications don’t work for them,” Dobbins said. The explosive growth in digital wallets is evidence of that. “Whether it’s Google or Venmo, or most recently the bank-led introduction of Paze into the market, growth was explosive.” Paze is a digital wallet developed by Early Warning Services LLC for online checkout.

Consumers also want choice in how they pay. “They want to pay the way they want to pay,” Dobbins said. “And we’re starting to see the introduction of new rails into our market.” Open banking is one of these new rails, and today 91% of consumers have linked their financial accounts to third parties, according to Dobbins. They do it to make it easier get loans and mortgages and to meet government financial obligations, but payment will absolutely be a part of this, he said. Cross-border money movement also is maturing into an easier and safer method, he noted.

The entry of real-time payments in the United States is another factor. The Clearing House Payments Co. LLC’s RTP network, launched in 2017, was joined last year by FedNow, the real-time payments network from the Federal Reserve. Dobbins noted that in many other markets real-time payments services fill in gaps that may not be as significant in the United States in some use cases.

Small businesses and how they enter the payment card networks is changing, too. “Now, we see an entire slate of informal merchants entering our payment system,” he noted, “and they’re being driven by the platforms and the expansive growth of mobile acceptance, and they’re entering the market and they’re not doing it in the traditional way.”

The expectations of small businesses demand more than payments alone, he said. They want services that can help run their businesses and that can help them attract and retain customers, make it easy for them to pay and be paid, and deliver faster settlement. They want better reporting and reconciliation, Dobbins said. “And, finally, they want us to deliver the security,” he said, “they’re thinking that they want to sell all the time, but they want to be protected in doing so.”

“The third topic is fraud,” he said, “and make no mistake, our business is all about trust. If we lose trust, we may never get it back.”

Synthetic identities, the use of deepfake profiles incorporating AI, and friendly fraud, or first-party fraud, are all troublesome for the payments industry, he said. It takes a concerted effort to counter fraud. “The first thing, and the one I’m most excited about, is we have to get out off our back foot. We have got more proactive here, offense versus defense,” Dobbins declared.

The fourth factor affecting payments is regulations at the federal and state levels. State legislation to require separate merchant category codes for gun sales means acquirers operating in these states have to modify their systems to accommodate that requirement.

Dobbins pointed to the Illinois Interchange Fee Prohibition Act as requiring changes beyond the simple face value of the measure, which prohibits assessing interchange fees on tips and sales tax.

“They effectively are asking us to re-architect our network to support this wall, and don’t get me wrong, even if we are able to do that, the work will pass on to each and every one of you. This would be an enormous, enormous activity,” Dobbins says.

At the federal level, Dobbins pointed to ongoing efforts to pass the Credit Card Competition Act, a measure that would compel offering credit card routing choice to merchants.

What can acquirers do about these challenges? Dobbins’ advice is to be active about these regulatory trends by working with trade associations to help legislators better understand the potential impact. “Make sure your message is heard,” he said. “So my call out to you is to be active as you see these regulatory trends.”